Securities law is highly complex and failure to comply with securities regulations may lead to civil and criminal sanctions.

Consult an attorney before trying to raise money. Even asking a potential investor for money can be considered a violation of securities law, unless you’re just applying for a regular business loan from your bank. Think of a security as a type of financial asset or investment. It represents ownership in a company or a part of a project and it can be used to finance your cooperative.

What is a Security?

Examples of security include stocks, bonds, derivatives, and many other types of financial assets. You create security when you ask people to put money into your business or venture, and you offer them a return. For example, a security could be:

- Selling stock in your business

- Asking people to lend money to your business

- Offering a share of your business profits interests in limited liability companies

It is important to know what is or is not a security because when you sell or even offer to sell a security, it needs to either:

- Be registered with the U.S. Securities and Exchange Commission and with the state agency where you want to raise money (in California, state registration is called “qualification”) OR

- Qualify for an exemption from registration. Registration/qualification is an expensive, time-consuming process. If possible, your business should try to find an exemption, which is simpler and less expensive.

Ways to Raise Capital With Securities

California Limited Offering Exemption

California Corporations Code Section 25102(f) offers a special securities law exemption to certain kinds of private securities offerings, if they meet the following criteria:

1.You must be exempt from federal securities filing requirements:

- Your company must be formed under California law (i.e., if you are a corporation you filed your articles of incorporation in California, etc.).

- You plan only to offer securities to California residents.

- Your contract with your investors includes that they will not resell the security to anyone outside the state for nine months.

- Your business is very California-focused – here is a test for this:

- You get at least 80% of your revenues from California.

- At least 80% of your assets are in California.

- You plan to use at least 80% of the money you raise within California.

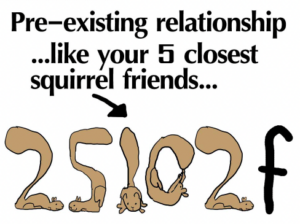

2. Then, you must meet the requirements for 25102(f):

- You can sell your securities to up to 35 investors that are not wealthy as long as they meet one or more of the following criteria:

- The investors have a preexisting personal or business relationship with you. These investors can be friends or family;

- The investors have enough financial experience to protect their interests; or

- The investors have experienced professional financial advisors.

- You can sell an unlimited number of securities to officers and directors of the company and accredited investors.

- 1) people with $1 million in net worth (excluding their home) or $200,000 in annual income, or

- 2) entities with more than $5 million in assets.

- Your securities offering cannot be advertised to the public. The investors must sign something saying that they are not investing for the purpose of reselling the securities to someone else.

- You have to file a simple form with the California Department of Corporations.

California Cooperative Equity Exemption

In California, there’s a rule called the California Cooperative Equity Exemption or the California Corporations Code Section 25100(r) that helps cooperatives raise money from their members without going through a lot of paperwork. Here’s how it works:

- A California cooperative can ask each of its members for up to $1,000 without needing to do a bunch of legal stuff. So, if someone wants to join the cooperative, they might need to put in $1,000.

- But, there’s a catch. If you buy into the cooperative using this rule, you become a member and get to vote on things. You can’t have someone who’s trying to make a profit, like a “promoter,” sell these shares for you.

- If you’re going to be actively managing the cooperative, the money you put in isn’t seen as a “security” (a fancy word for an investment), so you can contribute more than $1,000. This rule is mainly for members who won’t be running the cooperative. It is primarily for non-managing cooperative members that you would need to use the 25100(r) exemption.

Direct Public Offering (DPO)

Registering a DPO is not simple and it may require assistance from a lawyer, but it’s a nice option if you need to raise a lot of money and you want to offer shares of your business to local community members. A DPO is a securities offering that is registered at the state level and allows a business to publicly advertise investment opportunities to both accredited and non-accredited investors. Unlike an initial public offering (IPO), which requires an investment bank to underwrite the security, or the anticipated Crowdfunding exemption, which will require the online funding portal to be registered as an intermediary, a DPO allows an entity to sell securities directly to the public without a third party intermediary. Upon the state’s approval of your DPO plan, you can begin offering securities directly to the public.

The formation of a cooperative waste management company called CERO in the Boston area provides a great case study of a cooperative successfully raising money through different financing options. They have used crowdfunding, CDFI loans and a DPO to raise the money needed to purchase their trucks and enter into waste removal contracts. CERO hired Cutting Edge Capital, one of the leading consultants in the field of community capital development, to help them with launch their DPO. CERO reached its goal, raising $340,250 by early June 2015. All investments came from Massachusetts residents and ranged from $2,500-$25,00. Cutting Edge recently launched CuttingEdgeX (now SVX US), a marketplace which has provided a centralized place for investors to find social enterprises with open DPOs.

Angel Investors and Venture Capital

Finding an angel investor or venture capitalist to invest in your business can be competitive and challenging. At the same time, angel and venture capital funds have helped to launch and grow many successful businesses.

Socially Responsible Investing or Community Investment

Socially responsible investment organizations have grown rapidly over the past 30 years and continue to expand, even in the down economy. Many of them are located in the Bay Area.

Crowdfunding Exemption (2012 JOBS Act)

In April 2012, President Obama signed the Jumpstart Our Business Startups (JOBS) Act. Among other things, the JOBS Act includes a provision that would exempt certain small investments from securities registration requirements. Crowdfunded investing occurs when many members of the general public invest smaller amounts of money in a business. Instead of relying on a small pool of wealthy “accredited” investors, crowdfunded investing allows a business to gather support from their customers, neighbors, friends, family, and other community members, most of whom might be non-wealthy people who otherwise want to support your business. Although this new exemption is not specific to cooperatives, some cooperatives might consider using this exemption at some point, after considering related issues such as how crowdfunded investing might affect a cooperative’s governance or control by its members. Cutting Edge Capital is also a good resource for information on crowdfunding.

Related Articles

Other Financing Sources for Cooperatives

It might seem like there are limited ways to find funding for your business. Other than the conventional ways that include debt financing, equity financing and government financing there are alternative ways to raise capital including donations, micro-loans and bartering and more! Nontraditional Loans Micro Loans While traditional banking loans are sometimes difficult for cooperatives

Working With Lawyers During a Cooperative Conversion

While many conventional businesses operate and transact without much help from lawyers, cooperative conversions are perhaps uniquely in need of legal expertise and support. Lawyers can help you navigate the conversion process and protect everyone involved The reasons for working with lawyers during a cooperative conversion include: Cooperatives have unique governance, financial, and tax requirements