A business’ tax status determines how much income tax it pays and how that tax is calculated. The type of legal entity a business is formed under may influence the way its tax status is applied. There are a few different types of tax statuses a co-op can choose from that may be more advantageous or appropriate, depending on their choice of cooperative entity.

Definition of a Tax Status

Cooperatives come in multiple forms and have unique, and sometimes complex accounting, tax, and financing issues. A tax status is important to the overall flow of money and governance of the cooperative. Your tax status determines which tax forms you have to fill out and how many claims and deductibles you can take. Your tax filing status affects the total amount you pay in taxes.

Cooperatives are treated differently than traditional corporations and have their own specific tax rules. Taxation is complicated, and cooperative taxation is even more complicated. Businesses pay a variety of state and federal taxes (ie. excise taxes, unemployment insurance and temporary disability taxes, etc.) Here we will focus on federal income and employment tax.

Under federal tax law, cooperatives can deduct or exclude from their taxable income any amounts paid to their members as patronage dividends, which are similar to profit-sharing payments. This means that the income earned by the cooperative can be reduced by the amount of patronage dividends paid out to members.

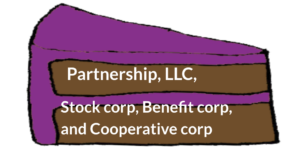

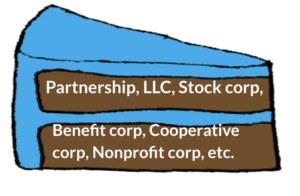

However, cooperatives also need to pay taxes on their non-member income, such as income earned from selling goods or services to non-members. The tax rate for this type of income may depend on the cooperative’s subchapter classification and the amount of income subject to tax.Below is a list of the different subchapter classification options

Tax status options

Subchapter T: Patronage Taxation

Under Subchapter T of the Internal Revenue Code, a cooperative can avoid some of the traditional corporate double-tax. This tax deductible is available to “any corporation operating on a cooperative basis”. Subchapter T allows for cooperatives to deduct the amount they pay in patronage refunds from their gross taxable income. Cooperatives function under a patronage-based profit sharing system. Unlike in a regular corporation, the surplus is distributed not based on ownership interest but on patronage. For example if the corporation is organized as a worker cooperative, “patronage” may be measured by work performed, including, but not limited to, wages earned, number of hours worked, number of jobs created, or some combination.

Subchapter C: Business Taxation

Subchapter C is the default tax status for corporations, as well as LLCs that elect corporate taxation. Earnings are double taxed meaning the corporation pays income tax on the net earning and the shareholders also pay income tax when they receive dividends of that net earning.

Subchapter K: Partnership Taxation

LLCs, partnerships, and Limited Cooperative Associations are taxed under Subchapter K by default (although these entities can elect to be taxed as a corporation). This tax status also allows for corporations to avoid double taxation at a federal level by using “pass- through” taxation. Meaning all income and losses are passed through to the owners and owners are considered self-employed partners. The main reason to choose this taxation is to avoid employee classification due to the immigration status of the member, assuming they structure the entity’s governance such that the owners are all equal co-owners and managers of the business.

Subchapter S: Pass-through Taxation

Subchapter S allows a corporate entity to avoid double taxation and pass through its gains and losses to the shareholders and it allows owners of an LLC to be treated as W-2 employees, rather than self-employed partners. Profit distributions would be taxed as ordinary income for the owners, rather than self-employment income like with a Subchapter K business.

Related Articles

California Worker Cooperative Entity and Tax Choice

When considering entity types for a worker cooperative, there are multiple options available. One possibility is to incorporate as a cooperative corporation if one exists under state law. However, it’s important to keep in mind that there are other options to choose from. To help make an informed decision, it’s helpful to consider factors about

Cooperative Governance: Fundamentals

Governance refers to how the company is controlled and how decisions are made. Governance also includes how the cooperative and its workers are held accountable, both to their internal members and to external stakeholders. There is an art to governance design, with many policies, practices, roles, and rules that can be arranged into place to

Legal Entities

When formed as a specific legal entity, cooperatives are able to legally enter into contracts and operate as a business. California recognizes several types of cooperative legal entities, each with their own structure and requirements. Other states may have have their own specific legal entities, so it’s important to understand the options available to you